Newsletter · May 17, 2026

Weekly Digest 20

PJM power-price pressure, the rise of AI deployment companies, and why the labor-market signal remains hard to read.

Topics we are tracking

PJM print: 76% year-over-year price increase

Source: Bloomberg — Data centers drive 76% rise in power bills on largest US grid

In Q1 2026 the wholesale power cost across PJM cleared at $136.53 per megawatt-hour, against $77.78 in the same period of 2025. The 76% year-over-year increase decomposes into a 398% rise in capacity charges, a 68% rise in real-time energy prices, and a 5% rise in transmission. The structural cause is locked in: 94% of PJM's forecasted peak load growth through 2030 comes from data centers, and the December 2025 capacity auction failed to clear sufficient supply for the 2027/28 delivery year for the first time in PJM's 25-year history. Customers in 13 states will absorb roughly $16.4 billion in capacity costs for that delivery year alone, against $2.2 billion in 2022.

The higher electricity cost itself does not change our view on data center economics. Power is a small fraction of total cost of ownership for hyperscaler facilities, where GPU capex, networking, real estate, and cooling dominate. A doubling of wholesale power costs moves TCO by low single digits and is fully passable to AI workload customers through inference and training pricing. Operators were already underwriting elevated power costs in their 2026-2030 capex plans. The wholesale print is confirmation of the assumption, not new information.

What matters is the second-order political response, which is now organized, bipartisan, and accelerating. The Trump administration and a coalition of PJM governors led by Pennsylvania's Josh Shapiro issued a joint Statement of Principles in January 2026 demanding action. AEP Ohio has already imposed a tariff requiring data centers to commit to paying for 85% of their forecasted load. PJM's independent market monitor has formally recommended that all large loads above 50 megawatts be required to bring their own generation or face curtailment during reliability events. FERC has not yet ruled, but the direction of regulatory travel is clear.

The build-out risk we are tracking is therefore not a power price risk but a permission risk. Supply chain bottlenecks in transformers, switchgear, and gas turbines were already pushing timelines out 12 to 36 months across the major equipment categories. State-level tariffs that shift cost back to operators, mandatory BYOG regimes, and outright moratoriums comparable to Denmark's recent grid connection pause add a regulatory delay on top of the physical one. Data centers have become the most visible local manifestation of an AI build-out that the median voter neither understands nor benefits from, and the political pricing of that cost has barely begun.

Linked stories worth following:

- Datacenter buildout in South America — Bloomberg: Petrobras completes first phase of $470 million data-center plan

- Economics of data centers in the UAE — Amelia K. Michael: Why the UAE

Deployment of AI

Source: OpenAI launches the Deployment Company

Deriving value from artificial intelligence remains one of the biggest issues for large-scale enterprises, as shown by the MIT study a few months ago. The headline finding was that despite nearly $40 billion in cumulative generative AI spending across the enterprise sector over the past two years, only 5% of organizations have demonstrated measurable business returns. The disconnect between what is technically possible and what most enterprises are actually using AI for is enormous. Outside of Silicon Valley and software engineering, where adoption is mature and ROI is visible in shipping velocity and code generation metrics, the rest of the economy is still struggling with the basics: identifying which workflows to target, how to redesign processes around model capabilities, and how to maintain systems that evolve faster than traditional software. Elad Gil captured this well in a recent tweet:

Anthropic, OpenAI, and Google are all investing heavily into initiatives that bring frontier models into enterprise workflows. A few examples worth flagging:

- OpenAI Deployment Company (May 11, 2026). A $10 billion pre-money Delaware LLC with $4 billion in initial capital from 19 investors led by TPG, with Advent, Bain Capital, and Brookfield as co-lead founding partners. McKinsey, Bain & Company, and Capgemini also participate. OpenAI retains majority ownership and super-voting control, has committed up to $1.5 billion of its own capital, and has guaranteed the PE syndicate a 17.5% annual return over five years. On the same day, OpenAI acquired Tomoro, a UK applied AI consultancy with roughly 150 forward-deployed engineers and clients including Tesco, Virgin Atlantic, and Supercell.

- Anthropic enterprise services firm (May 4, 2026). A $1.5 billion venture with Blackstone, Hellman & Friedman, and Goldman Sachs as founding partners, each committing $300 million alongside Anthropic. Additional backing from Apollo, General Atlantic, GIC, Leonard Green, and Sequoia. The structure mirrors OpenAI's approach: embedded engineers working inside mid-market companies, with the PE syndicate's portfolio companies as the initial client base.

- Google Cloud's enterprise AI push. Google is taking a different route, leveraging existing Workspace and Cloud relationships rather than building a separate deployment entity. The Gemini Enterprise tier announced earlier this year bundles agentic capabilities, custom model tuning, and Vertex AI deployment into a single enterprise contract. Less visible in the press, but the Q1 2026 Google Cloud backlog of over $460 billion suggests this is working at scale.

All three explicitly use Palantir's forward-deployed engineer model: technical staff embedded inside the client organization, working alongside business owners to redesign workflows around what models can actually do. The convergence on this model is not coincidence. It is the labs recognizing that frontier model capability alone does not produce defensible value capture. Where value accrues across the stack, closer to the model layer or closer to the application layer, varies by sector and is something we track closely.

Further reading:

- Goldman Sachs: Will the Corporate Investment in AI Pay Off?

- Stratechery: The Deployment Company, Back to the 70s, Apple and Intel

- OpenAI: Launching the Deployment Company

Labor market is hard to read right now

Source: BLS — Occupational Employment and Wage Statistics

We just spoke about the issues with AI deployment in large enterprises, so it is not surprising that we are not seeing a clear signal from the labor market right now. We are in a holding pattern. Headlines about company-specific layoffs that get highlighted as examples of "AI replacing jobs" can mostly be traced back to either overhiring during the previous cycle or company-wide underperformance. Coinbase and Block are good examples of this.

The doomer case mostly rests on the lump-of-labor fallacy. Historical evidence does point to productivity gains creating more jobs than they destroy. The agricultural transition took US farm employment from roughly one-third of the workforce in 1900 to under 2% by 2017 without producing permanent unemployment. Electrification raised labor productivity growth for decades while expanding the labor market rather than contracting it.

The problem is that every historical analogy played out over 20 to 50 years. The compression question is what matters now. If AI substitution happens over 3 to 5 years instead of decades, the absorption mechanisms that worked historically may not have time to operate. The political response cycle is shorter than the economic adjustment cycle, which means regulatory and protectionist intervention is likely to arrive before the new jobs materialise.

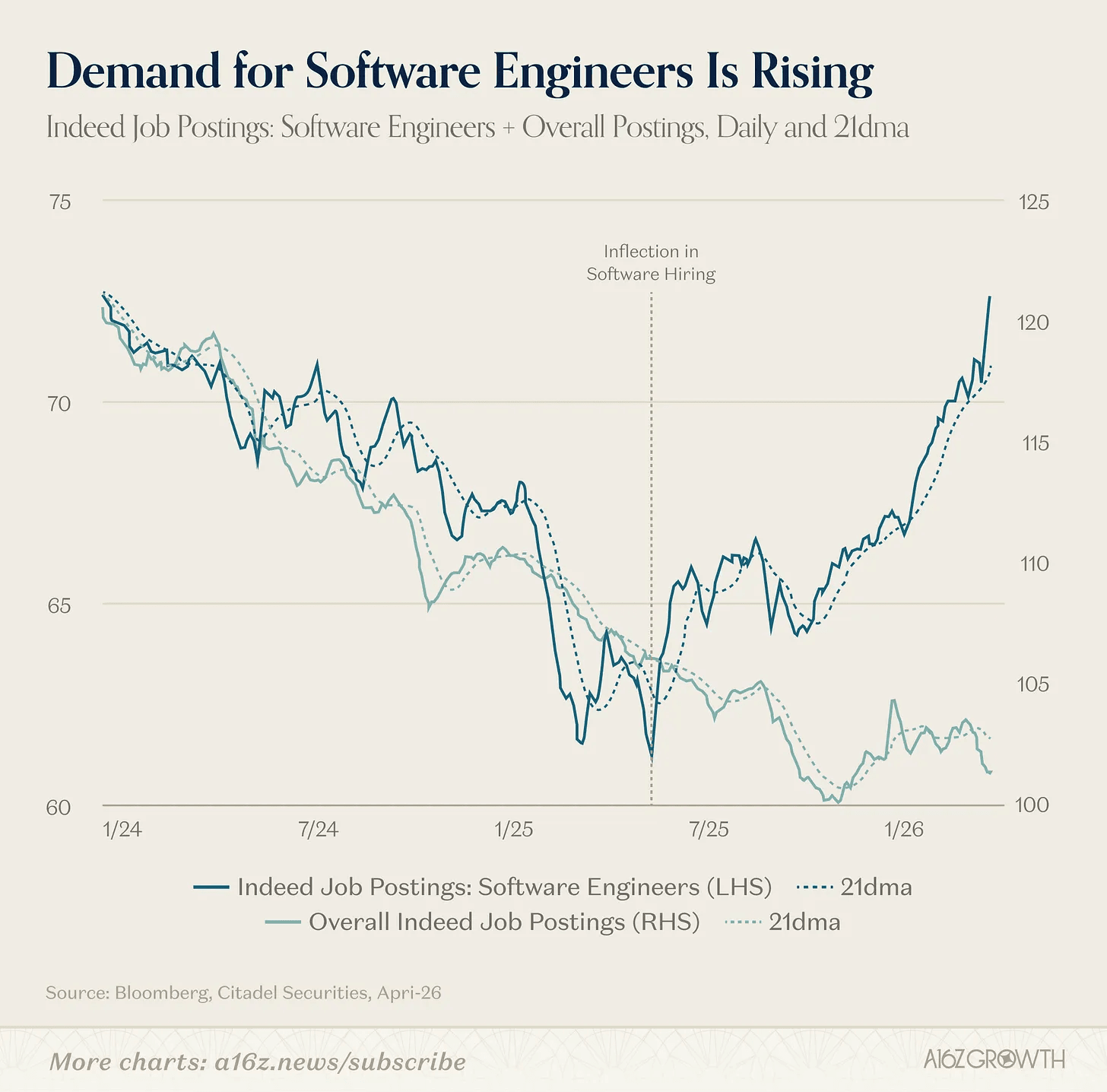

The aggregate data still looks fine. Initial jobless claims released May 14 came in at 211,000 for the week ending May 9, slightly above the 205,000 consensus but still historically low. Unemployment held at 4.3% in April. The four-week moving average for claims is anchored near 204,000. Sectoral data tells a different story. Crunchbase tallied at least 24,332 US tech sector layoffs in the weeks ending May 14, and the year-to-date pace is running at roughly 1,002 layoffs per day against 674 per day in 2025, a 49% acceleration in the underlying tempo. While at the same time Indeed job postings for software development jobs have been rising since 2025. This could point to a larger trend where software engineers might transition from tech companies into other areas of the economy as the AI diffusion is accelerating, but it's too early to have proof for this.

Entry-level jobs are perhaps the clearest signal of how AI could impact the labor market negatively. Stanford's Brynjolfsson, Chandar, and Chen documented in their November 2025 "Canaries in the Coal Mine" paper that early-career workers ages 22-25 in AI-exposed occupations experienced a 16% relative employment decline, controlling for firm-level shocks, while employment for experienced workers in the same occupations remained stable.

We expect a sharper contraction over the next 12 to 18 months as enterprise adoption moves from under 10% toward 30 to 50% and the deployment infrastructure discussed above produces measurable workflow substitution. We track BLS occupation-level series, entry-level hiring, and white-collar labor-share metrics, not aggregate unemployment.

Further reading:

- a16z: The AI Job Apocalypse Is a Complete Myth

- Stanford Digital Economy Lab: Canaries in the Coal Mine (PDF)

Seen on X

Other interesting stories

- Interconnects: Notes from inside Chinese AI labs

- Seoul Economic Daily: Labour strike at Samsung Electronics

- TrendForce: DRAM prices continue to surge in Q2

- FT: NATO to press European arms makers to boost investment

- Coatue: Public Market Update

- TechCrunch: Daniel Ek-backed Helsing to raise $1.2B at $18B valuation

- TechCrunch: Anduril raises $5B, doubles valuation to $61B

- The Information: Cerebras IPO winners include Foundation, Benchmark, OpenAI

- NYT: a16z emerges as biggest spender for the midterms