Newsletter · July 19, 2026

Weekly Digest 29

New York's statewide moratorium and New Mexico's block on Oracle's Stargate campus mark the moment politics — not water, land or power — becomes the binding constraint on the AI build-out, a risk we think is badly underpriced; Moonshot's Kimi K3 reaches the frontier as the largest open-weight model yet but stays too expensive and verbose to be a Sputnik moment, its real bite falling on frontier-lab margins rather than prices and pushing profit downstream to hardware and software; and China's biggest-ever chip IPO values DRAM maker CXMT near $85 billion, a price that confirms the memory shortage rather than threatening Samsung, SK Hynix and Micron.

Topics we are tracking

Politics becomes the binding constraint on data centers

Source: Axios — Hochul orders a one-year moratorium on large data centers

New York became the first state to impose a statewide moratorium on large data centers last week, enacted by Governor Hochul through executive order on 14 July after the legislature passed a one-year version in June. On the same day, the New Mexico State Land Office rejected, for the second time, the pipeline right-of-way needed to power Oracle's Project Jupiter, the roughly $165 billion Stargate campus being built for OpenAI. Opposition that had been confined to county zoning boards and utility commissions has reached the level of state policy, and in New Mexico it has halted a flagship project on a question of land access.

The case against data centers usually rests on three resources: water, land and electricity. Direct water use across all US data centers runs an estimated 17 to 20 billion gallons a year, a figure the EPA restated in 2025 and one the latest company disclosures bear out: Amazon reported its entire global fleet used just 2.5 billion gallons in 2025, and Google's data centers about 6.1 billion in 2024. Golf courses use 531 billion, residential lawns and gardens 2,920 billion, and crop irrigation 43,070 billion, so the country's golf courses alone use more than twenty times what its data centers consume. Land is similar. Data center buildings occupy an estimated 25 square miles, and full sites including setbacks perhaps 1,400, against close to 47,000 square miles of corn grown for ethanol and another 40,000 of idle farmland held in the Conservation Reserve Program. The physical footprint of the AI build-out is marginal against uses that attract no organised opposition.

Electricity is the more serious charge but the most widely misattributed. Residential rates have risen since 2020, but the PJM capacity-price increases are largely a product of how the market is designed. The base residual auction sets prices two years ahead on forecasts that have repeatedly overstated data center load, much of which was never built, and SemiAnalysis attributes most of the runaway pricing to this. A 2026 analysis even finds that data center growth from 2019 to 2024 held residential rates around 6% below a no-growth path, since large new loads spread fixed network costs across more consumption. The bill impact is real in a few zones and is being blamed on data centers almost everywhere.

Sites are also increasingly built behind the meter, with operators bringing their own generation, from on-site gas turbines to fuel cells, rather than adding load to the public grid. Oracle's switch from grid-tied turbines to on-site fuel cells at Project Jupiter is one example. The Trump administration has already moved to formalise this. Its March 2026 Ratepayer Protection Pledge had Amazon, Google, Meta, Microsoft, OpenAI, Oracle and xAI commit to build, bring or buy their own power and cover the full cost of the delivery infrastructure their data centers require, so that it is not passed to households. The pledge is voluntary and thin on enforcement detail, but the economics point the same way. Energy is a small part of a data center's total cost, under 10% by most estimates, while the servers are around 60%. Those GPUs depreciate on a fixed schedule whether the site is running or not, so a six-month permitting delay is far more expensive than the power bill it holds up, and operators will pay almost anything to avoid it.

There is a clear gap between the data and the sentiment on the ground, which makes this look more like political opportunism. Affordability is now a top voter concern, and a visible gigawatt campus owned by a large company is an easier target than an auction rule almost no one can explain. Data centers have also become a symbol of the concentration of wealth and power in a small group of tech founders while ordinary households pay more. That resentment runs across the entire political spectrum. Bernie Sanders on the left calls the industry's leaders "AI oligarchs" and has proposed a federal moratorium on new data centers. Steve Bannon on the right makes the same case against the "AI oligarchs" of Silicon Valley for abandoning ordinary workers. The data center is the physical thing that anger can point at, the part of the system a voter can see and a local official can stop.

Americans oppose a local data center — and most feel strongly

We think this is the most underpriced risk to the build-out. The political reality in the United States is an overwhelming public backlash against AI, from young people booing at commencement speeches to older workers who fear being replaced by it. As AI leads to more work displacement in the short term, this will likely intensify. And while the current administration has largely enabled business, at some point the Republicans won't be able to ignore the political reality.

Kimi K3 and the economics of the model layer

Source: Bloomberg — Moonshot Unveils Kimi K3 AI Model, Narrowing Gap With US Rivals

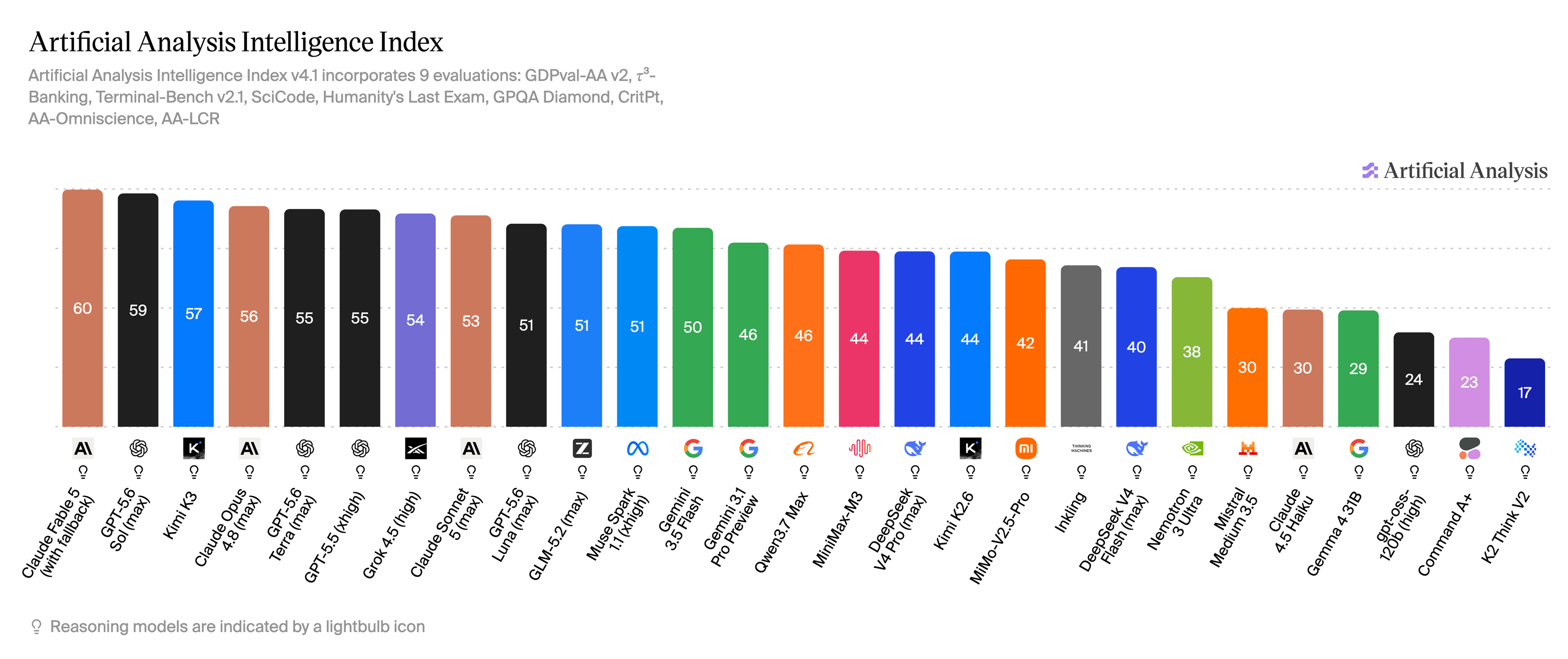

Moonshot released Kimi K3 on 16 July. At 2.8 trillion parameters it is the largest open-weight model built so far, and it ranks third on the Artificial Analysis Intelligence Index, behind Claude Fable 5 and GPT-5.6 Sol and just ahead of Opus 4.8. It also took first place on the Frontend Code Arena. For the first time, an open model that anyone can download from a Chinese lab is competing with the best Western systems on capability.

On price, though, K3 is less of a breakthrough than it looks. Moonshot has raised its rate card to $3 per million input tokens and $15 per million output, the same as Anthropic's Sonnet 5, so it does not undercut Western labs by a wide margin. It is also quite verbose: Artificial Analysis measured it using around 130 million output tokens on the benchmark, roughly twice the median for comparable models. That leaves its cost per task close to GPT-5.6 Sol rather than well below it. A real "Sputnik moment" would be an open model at the frontier that is also cheap to run.

It is an important model, however, because of how open competition impacts margins. A frontier held by two or three labs earning very high inference margins is good for those labs and poor for everyone else. They become the main buyers of power, data centers, semiconductors and cloud capacity, and in time they integrate down into those layers and up into the software built on them. Anything that raises competition at the model layer and pushes those margins down moves the profit outward, to power producers, chipmakers, hyperscalers, the neoclouds and the software firms building on the models.

This is why Nvidia is quite heavily invested in open weights. It sells the compute either way: an open model needs the same accelerators to run as a closed model of similar size, so wider use of open weights does not cost Nvidia any demand. It simply shifts the margin away from the labs and towards the hardware underneath them.

Open source is not the only thing that squeezes model-layer margins. Google, Meta and xAI make their money elsewhere, in advertising, cloud and their own platforms, so they can price their models cheaply without needing the model to be profitable on its own. Meta has openly stated that it is aggressively pursuing the cost frontier, and Google's Gemini models, while currently lagging in capability, have always been very cost-efficient. This drags the whole layer towards lower margins, the same effect open weights have.

We read K3 as a mild negative for the frontier labs and a positive for almost everything downstream of them. The negative is mild for now, for two reasons: the products and agent harnesses around Claude and ChatGPT may matter more to customers than the raw weights, and both labs may be using stronger internal models to build their next ones faster than rivals can follow, a loop that would compound any lead they hold. For the margin pressure to really bite, the market probably needs a more token-efficient open model at the frontier.

The aggressive push by every frontier lab into applied AI, through billion-dollar ventures with consultancies, banks and private-equity firms, suggests they already know the model alone will not hold the margin. Anthropic's $1.5 billion services venture with Blackstone, Hellman & Friedman and Goldman, and OpenAI's Deployment Company with TPG, Bain and Brookfield, are both bets that the durable revenue sits in deploying the model inside a business, not just in selling access to it.

China's biggest chip IPO confirms the memory shortage

Source: Reuters — CXMT's Shanghai IPO more than 200 times oversubscribed by retail investors

ChangXin Memory Technologies (CXMT), China's largest DRAM maker, is listing on the Shanghai exchange on 27 July, with investors placing orders from 16 July. At 8.66 yuan a share it raised about $8.5 billion, roughly double its original target and the biggest chip listing China has ever had. The price values CXMT at about $85 billion, or close to 300 times earnings against roughly 19 for Micron and 10 for Samsung and SK Hynix. It is the fourth-largest DRAM maker in the world.

Most people see a new Chinese memory maker and assume it will flood the market and push prices down, the way China did in solar, steel and older chips. However, this seems unlikely given that in the first quarter CXMT's prices were only 5% to 10% below Samsung, SK Hynix and Micron, and its cost to make a bit of DDR5 was more than 30% higher than theirs. It is not undercutting anyone. It sells at the same high prices as the three incumbents do and earns less on each chip.

First-quarter revenue reached about $7 billion, up roughly 700% on the year, at an operating margin near 70%, and the growth came almost entirely from price. Bit shipments rose 11% in the quarter while selling prices rose 57%, following even larger increases in the two quarters before. The market is in a once-in-four-decades shortage and DRAM prices are expected to roughly double again this year. Even after modelling the new wafer capacity from CXMT and everyone else, DRAM remains undersupplied into 2028, because fabs take years to build and no single player can accelerate fast enough to close the gap. CXMT's share of global bit shipments rises from about 9% in 2025 to 12% in 2027 on their numbers, meaningful in a market approaching $1 trillion but not enough to break it.

Almost all of CXMT's output is commodity DDR and LPDDR. HBM is a rounding error, and the reported yields for its first HBM3 stacks are only around 25%, one to two generations behind the frontier. China's drive for compute self-sufficiency will push CXMT towards HBM over time, but that is a multi-year effort, and for now the high-margin HBM franchise that carries SK Hynix in particular stays with the three leaders. Domestic demand also has first claim on what CXMT can make: it is effectively sold out, with Alibaba, Tencent and Xiaomi on its cap table and Beijing treating its output as a strategic asset. Even Apple, which is testing CXMT chips and lobbying Washington for clearance, is only qualifying them for phones sold in China, not its global build. CXMT also still trails all three leaders on scale, with 2025 DRAM revenue near $8.6 billion against Samsung's $72 billion, SK Hynix's $52 billion and Micron's $37 billion.

Global HBM wafer capacity

- Samsung

- SK Hynix

- Micron

- CXMT

This listing and its price are a sign that the structural shortage in memory chips is continuing. Investors are paying a high price for CXMT, which tells you they expect memory to stay tight. This is good for Samsung, SK Hynix and Micron: a new rival is selling at the same high prices they are, and the most profitable product, HBM, is the one CXMT is furthest behind on. The future of AI is inherently hard to predict, and CXMT could still become a threat later this decade, once it has enough capacity and good enough HBM to move the market. For the next two years, though, that day looks a long way off.

Seen on X

Other interesting stories

- Thinking Machines: The Future Worth Building Is Human

- Axios: Demis Hassabis, Google DeepMind, and AI regulation

- Jerusalem Post: US uses one-way attack sea drones against Iran for first time, CENTCOM says

- Cerebras: How We Built Our Knowledge Base

- ChinaTalk: China's Mythos Moment

- Contrary Research: Are Prediction Markets Doomed to Fail?

- The Free Press: Tyler Cowen — A Dangerous Turn in AI Regulation

- The Information: DeepSeek's Annualized Revenue Nears $500 Million, Boosting Fundraise, IPO Plans